What’s Next for BaaS: Revisiting Risk, Infrastructure, and Channels

Banking-as-a-Service (BaaS)1 is in hot water. Once a favored path to innovation, especially for community banks, the model is now attracting heaps of negative attention due to an array of business stability and compliance issues. As a result, BaaS sponsor banks and their partners are increasingly facing business challenges and regulatory actions, pushing them to revisit their operations, pivot their strategies, and in some cases, drop out entirely.

To be clear, the industry’s issues shouldn’t cast a shadow over BaaS overall. These problems are not signs that there’s something fundamentally wrong with BaaS. A BaaS line of business can still be successful. At its most basic, it may help a bank gather deposits with a low cost of customer acquisition and earn platform fees, transaction fees, and interest. But the recent turmoil points to how important it is to be self-honest and diligent about the development of a BaaS strategy.

The BaaS market at a glance

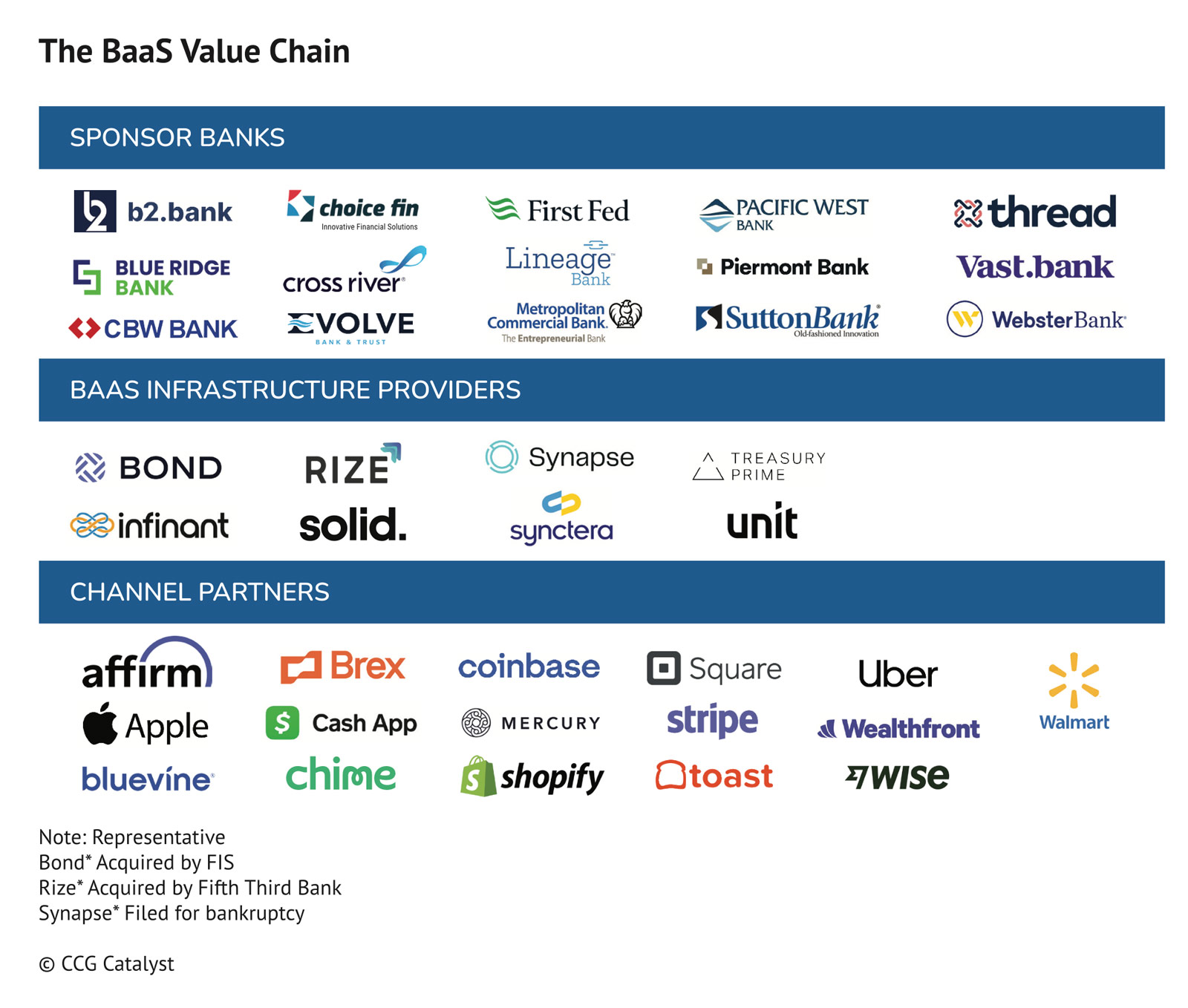

The BaaS value chain is made up primarily of three types of companies:

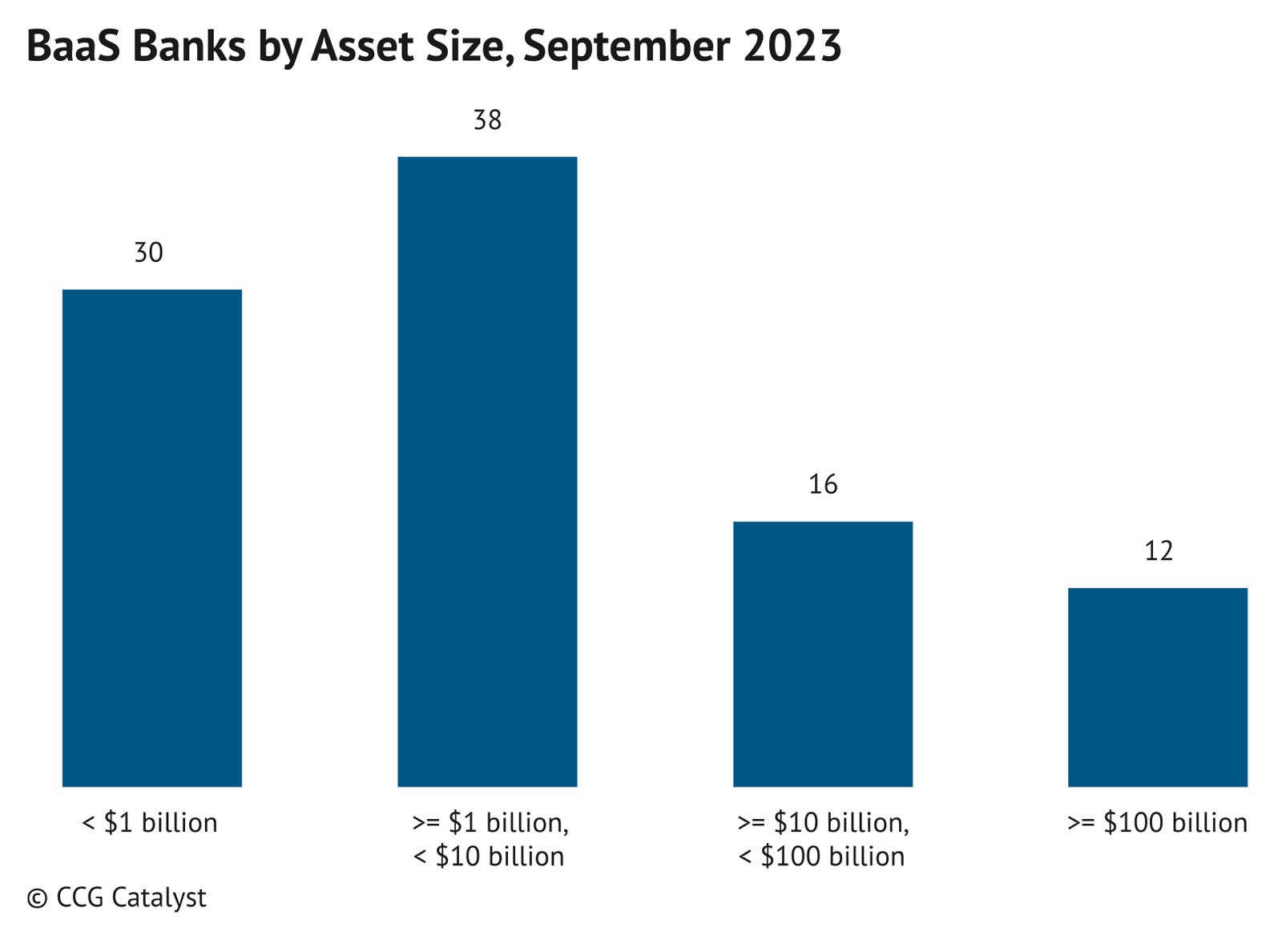

- Sponsor banks. Sponsor banks are a mix of financial institutions (FIs) ranging in size from less than $1 billion in assets to more than $100 billion. About 70% fall under the exemption from the Federal Reserve’s $10 billion cap on debit card interchange fees, but many are far smaller: about 60% have assets under $5 billion and about 30% have assets under $1 billion.2 A common model for under-$10 billion BaaS banks is to gather deposits by providing deposit products and earning processing fees from debit card swipes and network sponsorships.3

- BaaS infrastructure providers. Infrastructure providers are vendors that facilitate a BaaS business with technology that a sponsor bank would find difficult or impossible to build on its own. They provide a platform or technology that BaaS customers use to connect to the sponsor bank’s services and ancillary features that may for example include KYC, AML, and fraud management. They may also double as a matchmaker, but that setup is receding amid rising regulatory scrutiny and demand for greater oversight.

- Channel partners. Channel partners are nonbank customers of sponsor banks that embed financial products and services into their own solutions. They’ve often been consumer fintechs, but B2B2B fintechs are now attracting more investment as the consumer fintech market tightens amid a tough capital environment.4 The channel partner category is also shifting to nonfinancial companies.

Banks are ultimately responsible for third parties’ risk and compliance behaviors.5 Risks to the bank crop up when a sponsor bank works with a new partner. With a BaaS program, those partners can quickly multiply. The more partners a sponsor bank has and the further removed they are from the bank’s direct oversight, the greater risk the sponsor bank faces from operating a BaaS program. Infrastructure providers also have their own technology partners, which makes it even more complex for sponsor banks to vet and oversee third parties.

What went wrong with BaaS

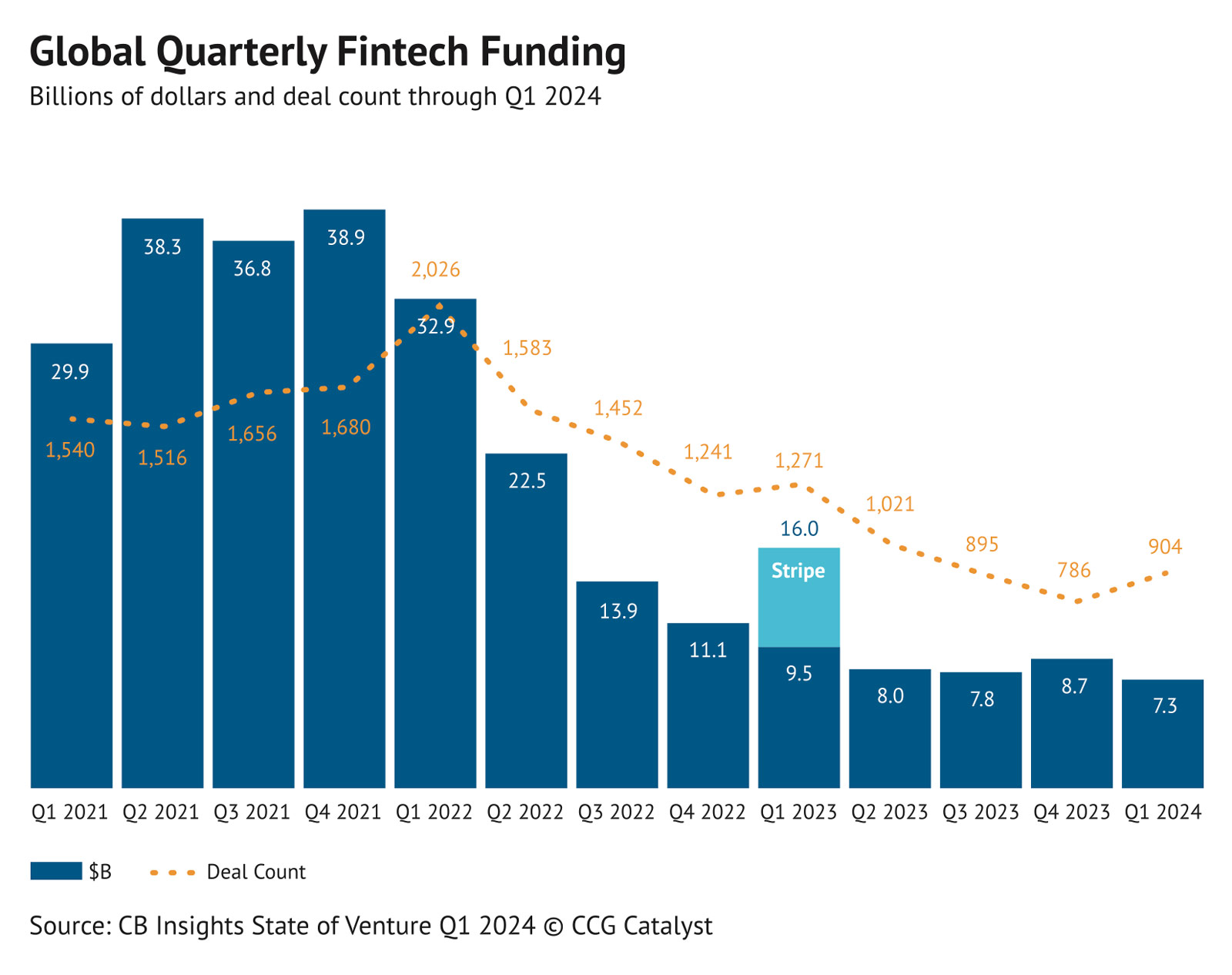

BaaS exploded with the fintech industry, especially in 2020 and 2021 as funding hit record highs. As one senior executive at a BaaS bank told CCG Catalyst, “Everybody wanted to be part of the next hot fintech.” Then, fintech funding collapsed, and investors soured on the “growth at any cost” strategy. The fall in funding between 2021 and 2022 drove a rapid contraction in the consumer fintech space,6 where many BaaS customers came from. That pullback hurt BaaS sponsor banks and infrastructure providers.

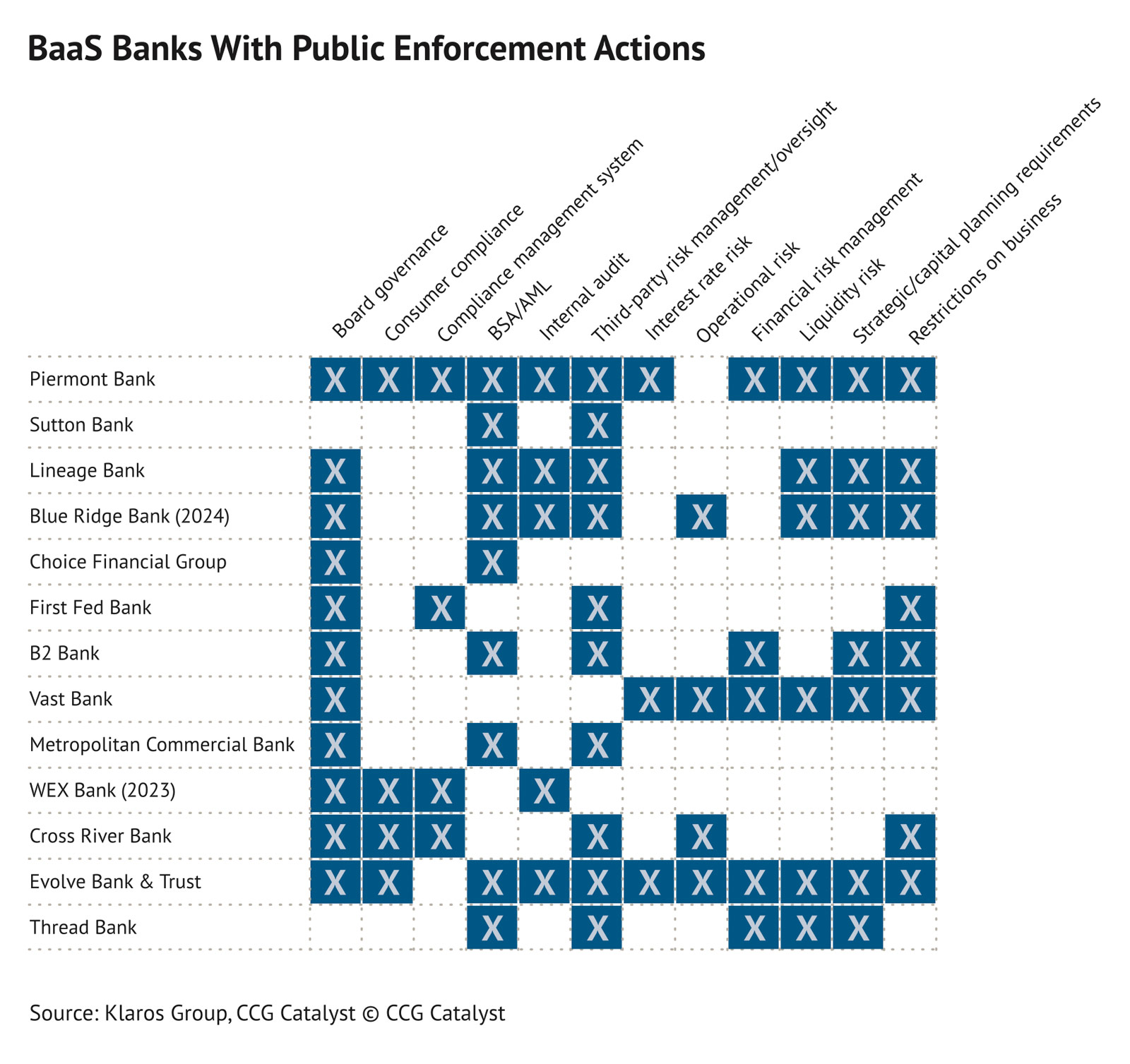

At the same time, cracks in compliance and oversight (at least in part because of the gold rush) began to emerge.7 Regulators by now have cited sponsor banks for a range of issues, including deficient board governance, third-party risk management, and BSA/AML, stemming from relationships with fintechs. As of May, 13 BaaS banks had been hit with enforcement actions from their primary federal regulator, sometimes more than once.

In response to these problems, BaaS thinned out and consolidated:

- Sponsor banks dropped fintech partnerships or announced plans to exit BaaS. Metropolitan Commercial Bank is shutting down its BaaS operation due to the compliance burden,8 and Blue Ridge and Lineage Bank both appear to be winding down their fintech relationships.910 CBW Bank is reportedly trying to sell itself.11

- BaaS infrastructure providers thinned out and restructured. Bond sold itself to FIS, Rize Money sold itself to Fifth Third,12 and most recently, Synapse filed for bankruptcy.13 Layoffs among these providers were widespread,14 and, as mentioned, many are taking steps to reduce the role they play between sponsor banks and fintechs.15

- There have also been public spats between banks, BaaS infrastructure providers, and fintechs. Evolve Bank & Trust and Synapse blamed each other for lost customer funds,16 and Synapse and the fintech Mercury have fought over money and breach of contract.17

Overall, BaaS grew too fast when the fintech market was doing well. That led to lapses in judgment and oversight that later became obvious. Now, the industry is recalibrating as regulators catch up to the scope, size, and intricacies of BaaS. Regulatory action isn’t a surprise given the novelty of BaaS as regulators work to understand the business model and the market, said several people CCG Catalyst spoke to. “The fact that there are enforcement actions is inevitable,” Remy Carole, COO at Treasury Prime, told CCG Catalyst. “This space is evolving.” But regulatory actions on today’s scale weren’t guaranteed: “We would not have this mess if [intervention from regulators] had happened sooner,” Jason Henrichs, CEO of Alloy Labs, said.

Moreover, it’s become clear that not all banks are up to the challenges of BaaS. “Many banks have gotten and will get into some form of enforcement,” said a senior executive at a BaaS bank. “The question is more so who comes out of it and who is serious enough to enhance the infrastructure, processes, and people to make this work in a very robust way.” Under the threat of regulatory action, banks are “trying to work backward from the enforcement actions” and third-party risk management guidance, Itai Damti, CEO of Unit, told CCG Catalyst.

The way forward for sponsor banks

Problems for BaaS have almost always been rooted in poor controls for a sponsor bank’s fintech strategy.18 “What’s frustrating to me […] is that if I look at the landscape of banks that are running into trouble, the root cause of what happened in most [cases] is that [the] financial institution got over their skis,” said a senior executive at a BaaS bank. “They failed to make the forward investment,” he said, adding that they often did not understand the business well enough or assumed too much about the role a technology partner would play in compliance.

A well-managed, competitively positioned BaaS line of business should enhance the growth and margins of a committed and properly prepared sponsor bank. The upfront work — most importantly, dedicated leadership, planning, and resources for BaaS risk and compliance — is fundamental. As sponsor banks and potential new entrants contemplate their next moves, understanding that will be critical. This is not a place in which to dabble.

For those who truly commit, there are three elements to address:

- Due diligence and enforcement. Proper due diligence demands that sponsor banks have close, bilateral relationships with channel partners. They need to acutely understand what their partners do, that those partners have appropriate risk and compliance policies, that they strictly enforce those policies, and that they independently engage with regulators. Banks should vet BaaS infrastructure providers as critical vendors and treat channel partners with a greater level of risk than the bank technology they use to acquire customers directly.

- Business vision, expertise, and scale. High payments volume, low infrastructure costs, sticky deposits, a stable customer base, high-margin deployment of deposits, and product or technology leadership all play into a BaaS bank’s success.19 It’s also crucial that a BaaS bank’s board includes expertise in compliance, risk management, governance, audit, and technology, and hires senior management that meets those obligations.

- The right BaaS stack. Readiness for BaaS-driven growth depends on a technology stack that efficiently and compliantly supports programs, limits vendor dependencies, and facilitates the bank’s direct oversight of channel partners. “We can outsource the technology but not the compliance responsibilities,” Jason Wessling, president and CEO at Pacific West Bank, told CCG Catalyst. In that model, a vendor provides the infrastructure and critical services to support BaaS programs while the sponsor bank negotiates and manages programs. “The banks need to see all the way down to the end customer via their partners intraday and mirror and settle to the operating accounts,” said Mitchell Lee, chief risk and compliance officer at Synctera.

There’s still an opportunity for those who take the time to get it right. By one estimate, financial services embedded into ecommerce and other software platforms accounted for $2.6 trillion in US financial transactions in 2021, a number that’s forecast to exceed $7 trillion by 2026.20 But sponsor banks should not underestimate the commitment it will take — they must invest robustly in a well-thought-out, comprehensive BaaS strategy. As a result, today’s pool of sponsor banks will most likely consolidate into those that make BaaS a core competency.

Our outlook

For the BaaS market as a whole, trends in partnership preferences show how BaaS is moving on from the fintech bubble. “If we look at a company that tells us they’re going to launch a consumer neobank, that’s probably not going to work,” said a senior executive at a BaaS bank. The way “BaaS” is branded is also changing. Embedded finance, the distribution channel, appears to be an increasingly popular term, according to our discussions with the industry.

We expect to see the following:

- Banking products will become one of a handful of features among many within software solutions. “Financial services are going to become commonplace and less visible to regular users,” said Treasury Prime’s Carole.

- The median size of sponsor banks will change. Sponsor banks above the $10 billion exemption from the Regulation II interchange cap may be best-suited to enterprise-scale embedded finance.

- Small sponsor banks under the $10 billion cap will specialize, consolidate, scale, or exit the market. Specific outcomes will vary based on specialization, the distribution of customers, and the choice of channel partners.

- Sponsor banks will demand that infrastructure and channel partners meet stringent risk and compliance obligations, including robust technical capabilities for implementing and operating banking products.

Embedded finance is playing out from the ground level up. Ninety percent of the deals Unit closes today are with software companies, and 10% are with legacy fintechs, the opposite of several years ago, said Unit’s Damti. Software examples are increasingly abundant. Some include:

- Toast, which offers small business loans21 in addition to its payments and business management services for the restaurant industry.

- Square, which offers small business banking22 in addition to merchant services.

- Stripe, which offers loans to small businesses23 and its own BaaS API24 in addition to merchant services and payment processing solutions.

- Shopify, which offers banking and lending services, including a checking account built into its seller platform and various lines of credit for merchants.2526

Embedding banking and payments into software solutions isn’t the only end game. Working with large commercial clients in general would lower the risk for sponsor banks, said several people. An example might be accounts integrated with large employers’ payroll services, Chris Siemasko, COO at Infinant, told CCG Catalyst. “Understanding [a] vertical gives you the advantage of being able to know the ins and outs of where that company is headed and the products they need to serve their customers,” added Synctera’s Lee. Sponsor banks also have low-risk, classic white-label opportunities from prepaid cards via gift cards, transportation cards, government disbursements, insurance payments, and spending cards.

The BaaS industry’s recalibration is healthy and important to its long-run success. Once the dust settles, risk and compliance for BaaS will have normalized. Regulators will have a grip on BaaS, including the nature of third-party risk, and they’ll understand how to address issues proportionately with sponsor banks. With clear and comprehensive regulatory guidance, participants in the BaaS value chain will have a more precise idea of how to meet their obligations. Infrastructure providers will move on from partner matchmaking to focus on BaaS-enabling technology. And as sponsor banks consolidate and scale, they’ll bring the partner lifecycle further in-house.

©CCG Catalyst 2025 – All Rights Reserved

No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage and retrieval system, without prior permission in writing from the publisher.

Download a PDF of this article