New Frontiers in Banking 2024: Balancing Caution and Excitement

After years of excitement and fervor around novel ideas in banking like Banking-as-a-Service (BaaS) and crypto, the industry is recalibrating. This is largely in response to a tightening regulatory environment and the very public failure of a number of these ventures. However, caution doesn’t necessarily mean lack of interest; in fact, much of the conversation around innovation, and especially artificial intelligence (AI), remains quite optimistic. So the question leaders should be asking then is, “What exactly is relevant and important to pay attention to?”

This report is designed to help bank executives figure that out, to help them understand what innovations dominate today’s discourse and where they’re headed. It is based on CCG Catalyst’s New Frontiers Survey 2024, which asked C-level bank executives in the US about their attitudes and priorities in the current environment. It’s a fresh look at the topics covered in last year’s New Frontiers report, which builds on a section in CCG Catalyst’s periodic Banking Battleground report.

Methodology and purpose

CCG Catalyst surveyed 114 C-level bank executives between April and May 2024 to gauge their attitudes and perspectives on today’s operating environment with an emphasis on technology, innovation, and new areas of opportunity. As part of our analysis, we’ve divided the key findings from this survey into three sections: technical readiness and expectations, new business frontiers, and new technology frontiers. The frontiers we’ve chosen represent only a subset of opportunities; we’ve focused on these because of their importance to strategic planning. The survey data is unweighted, and the analysis that follows is based on our sample.

Technical readiness and expectations

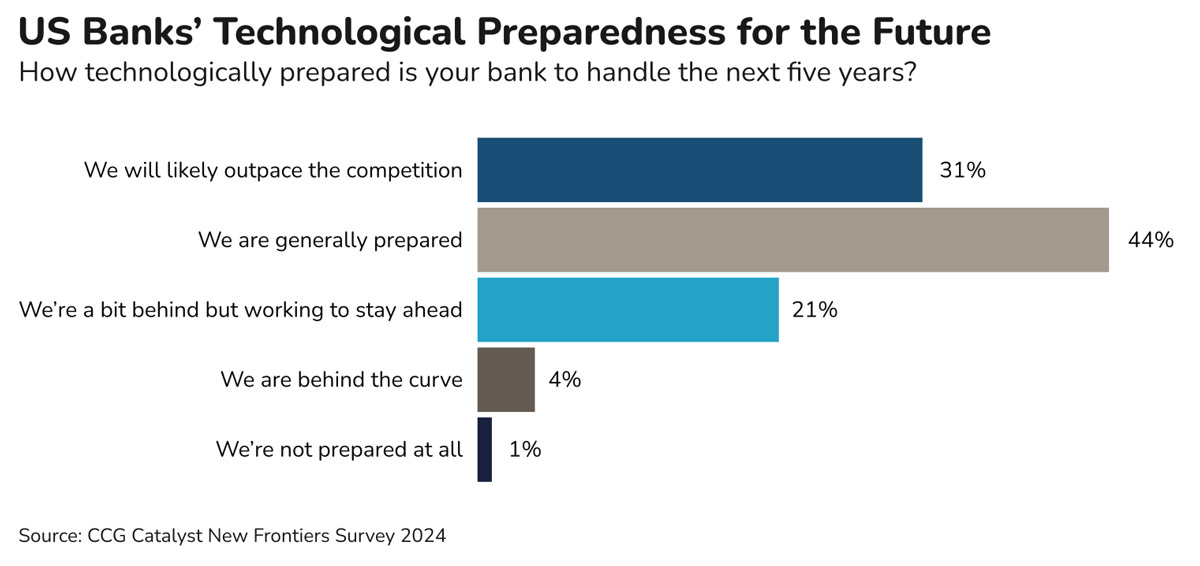

Modernization forms the foundation for the technical flexibility and operational sophistication needed to innovate. In our survey, almost half of respondents claimed their business was generally technologically prepared to handle the next five years, and 31% said they would likely outpace the competition. These results were little changed from last year, suggesting consistent comfort and confidence with technological preparedness year over year. But it can be too easy to get caught up in a rosy idea of technical readiness or use too narrow of a lens to assess customer needs and the state of competition.

It’s prudent for bankers to grasp the technology practices they should reinforce and the changes they should make. Commitment to innovation, a philosophy that favors best-of-breed solutions, and productive relationships with fintechs are crucial. Relationships with fintechs within the context of a bank’s business strategy will influence its technology stack’s flexibility and the institution’s ability to quickly evolve. Some respondents leaned toward a best-of-breed strategy for technology selection: 28% of respondents said less than 25% of their core, digital, electronic funds transfer (EFT), and payments technology came from a single company. And 55% of respondents said working with fintechs was an integral part of their business strategy.

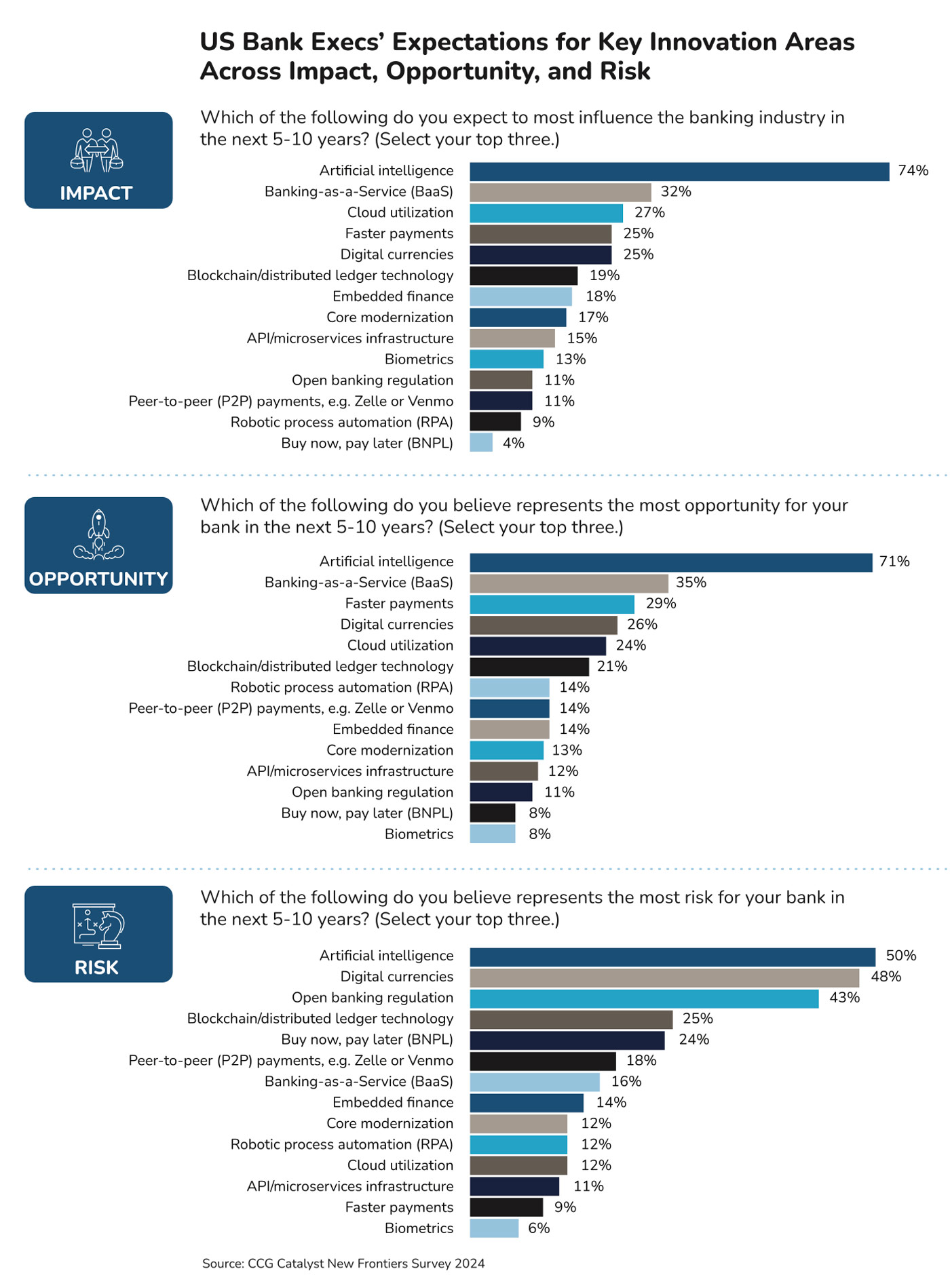

To get an idea of which trends bankers believed would have the greatest impact, create the most opportunities, and pose the greatest risks, we asked respondents to select their top three in each bucket:

- Impact: The top area of influence in the next 5-10 years, according to respondents, will by far be AI — followed distantly by BaaS. They were also ranked first and second last year, but the gap between them widened — AI led BaaS by 42 percentage points in this year’s survey, increasing by 15 points, while BaaS fell by 10 points. Digital currencies deflated from 32% to 25% and third to fifth, and cloud utilization jumped from 16% to 27% and eighth to third.

- Opportunity: AI, BaaS, and faster payments returned as the top three, although AI was a dramatically more popular choice. AI jumped 17 percentage points, from 54% to 71%, while BaaS fell by nine percentage points. The result for faster payments was little changed.

- Risk: AI, digital currencies, and open banking regulation clustered at the top. AI increased from 44% to 50%, digital currencies rose from 43% to 48%, and open banking regulation grew from 33% to 43%. The values for blockchain/DLT and BNPL were little changed and came in far behind.

Key takeaways:

- AI was nearly all-consuming. Enthusiasm for AI and wariness of its risks continued. AI was the most popular opportunity and factor most likely to influence the banking industry over the next 5-10 years by wide margins, and it was ranked the top risk by marginally more respondents than for digital currencies.

- The star power of BaaS faded. The fall in perceived impact and opportunity likely reflected this year’s compliance and third-party risk crisis and a more careful attitude toward the model. The short-term impact of BaaS played out with the decline of consumer fintech, revealing it isn’t actually an easy path to growth. 1

- Open banking was almost exclusively rated a risk. The Consumer Financial Protection Bureau’s (CFPB’s) open banking rule is just around the corner, and respondents likely dread compliance. Open banking also poses an opportunity, but with regulatory pressure, it may not feel that way.

![]()

New business frontiers

Now that we’ve explored respondents’ high-level perspectives, we’ll dive into how executives perceive specific areas of innovation in banking. This section, which focuses on business opportunities, looks at new frontiers in how financial services are constructed and delivered and how banks operate. We take a deep dive into BaaS, embedded finance, bank-owned marketplaces, banking for cannabis-related businesses, and sustainability strategies.

Construction and delivery

BaaS

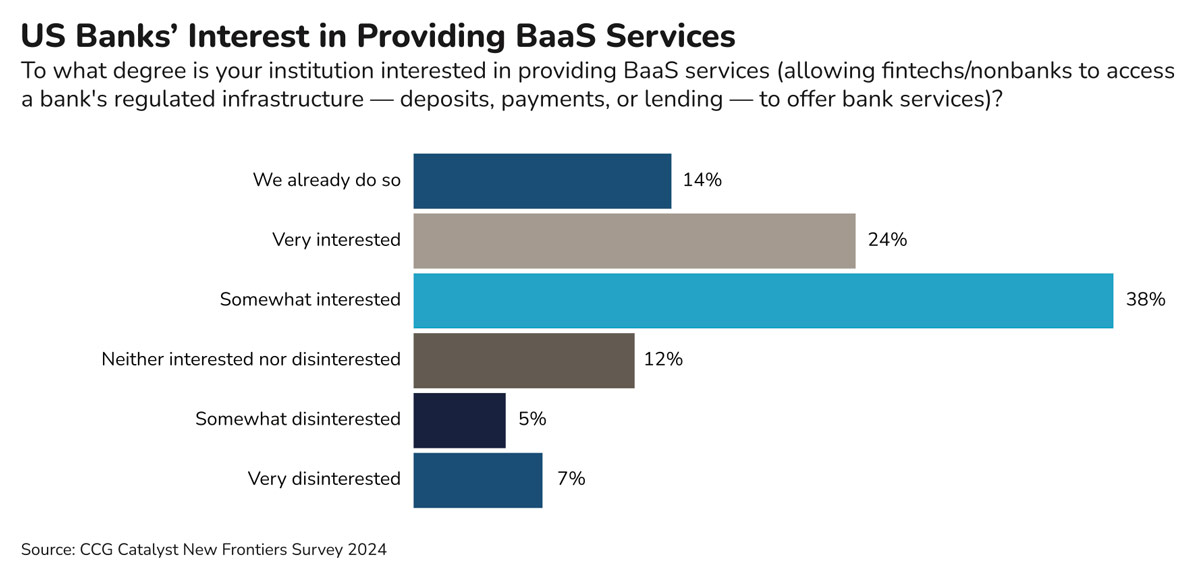

Respondents’ fervent interest in BaaS waned this year: Nine percentage points fewer respondents were “very interested” in providing BaaS services than in last year’s survey, and those who were “somewhat interested” rose eight percentage points from 30% to 38%. The number of respondents who were “neither interested nor disinterested” or below rose seven points, from 15% to 24%.

This data likely reflects the business challenges and regulatory scrutiny BaaS sponsor banks and their partners have faced after BaaS grew too fast in a hot market for fintech. That rapid growth led to glaring risk and compliance lapses and regulatory action. 2 It’s become clear that not all banks are up to the challenges of BaaS, and sponsor banks shouldn’t underestimate the commitment it will take. A well-managed, competitively positioned BaaS line of business should enhance the growth and margins of a diligent sponsor bank. Upfront work — most importantly, dedicated leadership, planning, and resources for BaaS risk and compliance — is fundamental.

Embedded finance

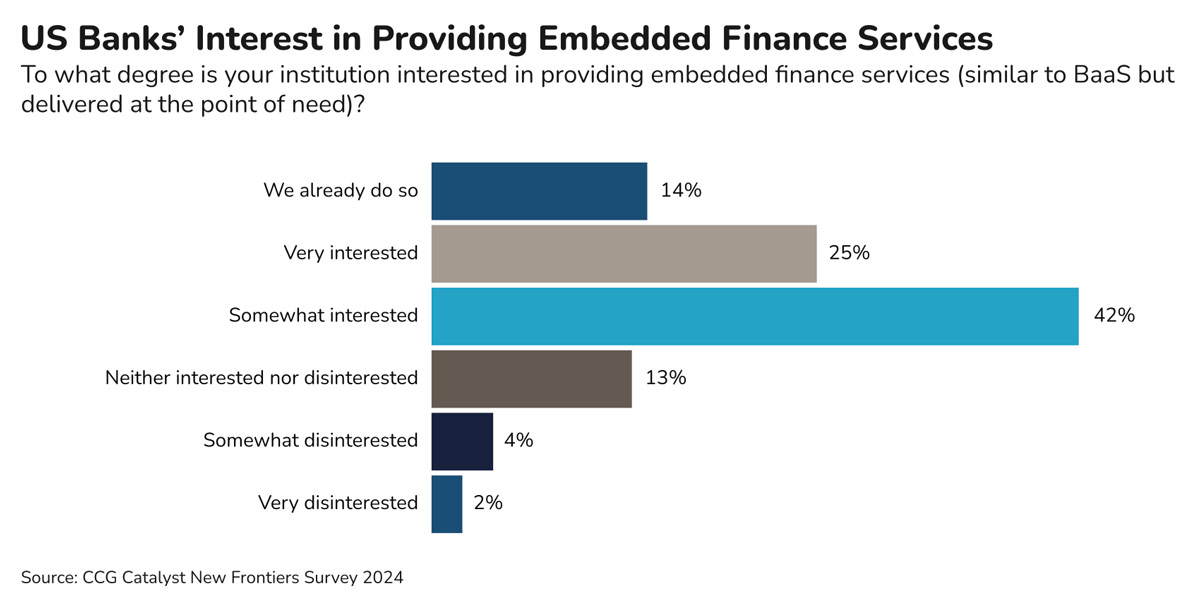

Embedded banking, a form of embedded finance, is the delivery channel for BaaS. As such, the change in respondents’ interest in embedded finance roughly tracked attitudes about BaaS. Those who were “very interested” fell eight points from 33% to 25%, while “somewhat interested” rose seven points from 35% to 42%. The number that was “neither interested nor disinterested, “somewhat disinterested,” or “very disinterested” was 19%, up slightly from 16% last year.

Embedded banking is an exciting concept — banking products and services delivered through nonbanks, like technology companies, business management software, ride sharing, and marketplaces. It’s increasingly the lens through which the industry sees financial services provided as a service. 3 But embedded banking poses the same risks to banks as BaaS, and from the bank’s perspective, requires a level of commitment and investment that for many has made BaaS less attractive.

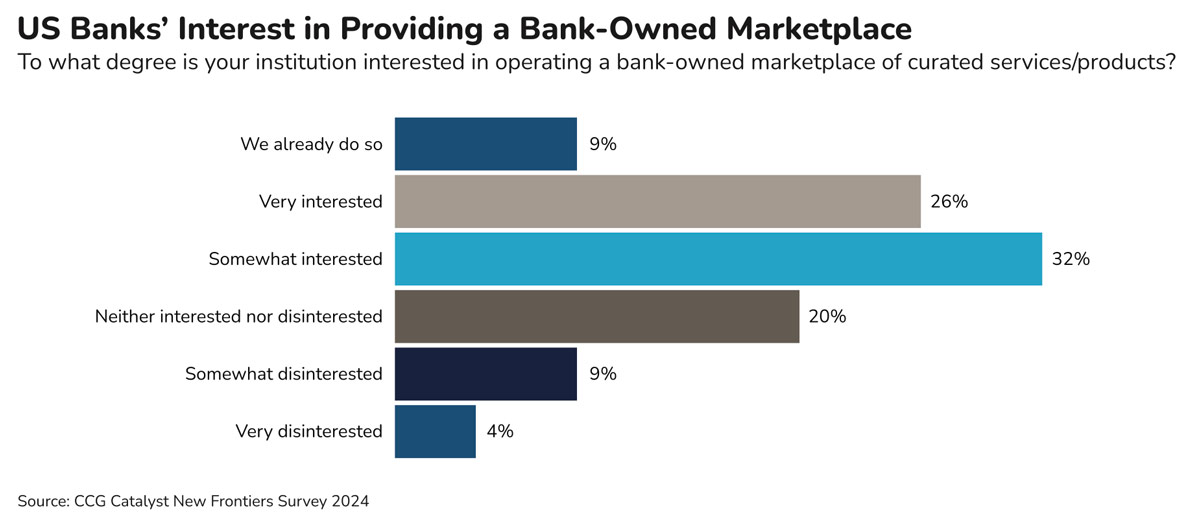

Bank-owned marketplaces

A bank-owned marketplace allows banks to offer third-party products or services through in-house digital experiences. Strong interest in bank-owned marketplaces fell: Respondents who said they were “very interested” in operating a bank-owned marketplace dropped from 40% in last year’s survey to 26% this year, while the percentage that was “somewhat interested” stayed about the same (34% to 32%). Those who were at best “neither interested nor disinterested” rose from 18% to 33%.

Will a retail bank embed third-party services in its digital banking tools and sell financial products that aren’t its own? That depends on what retains and engages its customer base — the bank’s own properties, branded technologies, and products, or the availability of third-party offerings. It also depends on how sophisticated a bank makes its in-house digital experience, the breadth of products it offers, and how comfortable it is with enabling customers’ access to nonproprietary products and services. Nonbank platforms with embedded financial services make bank-owned marketplaces for in-house and third-party products and services less compelling, however, because the most relevant financial products at a point in time are distributed at the point of need.

New ways of operating

Cannabis banking

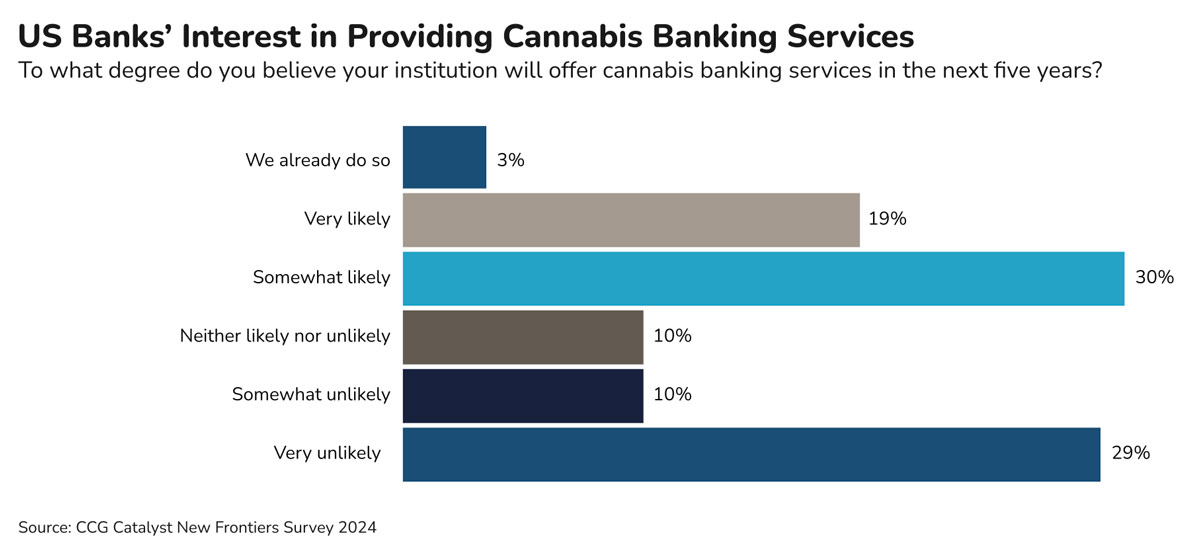

US banks have been in limbo with the legality of banking cannabis companies and their service providers, and few have taken the plunge into that line of business. Respondents to this year’s study appear to have made firmer decisions than last year’s sample about offering or not offering cannabis banking services.

A tiny sample (3%) said they already offered cannabis banking services, which changed little from last year’s survey. The proportion who said offering cannabis banking services was “very likely” edged up (from 15% to 19%). With legal clarity in sight, some bankers may be getting more comfortable with the idea; others have decided against it. The biggest upward moves year-over-year were for the respondents who said it was “somewhat likely” (19% to 30%) and “very unlikely” (19% to 29%).

Without protections from liability, the American Bankers Association has argued, banks will be reluctant to serve the cannabis industry. 4 Legislation may change that. A bill that cleared the Senate Banking Committee earlier this year would explicitly allow financial institutions (FIs) to handle money from state-licensed cannabis businesses and their service providers. It would also allow them to accept deposits and make loans to employees of those businesses. 5 This bill, if it became law, wouldn’t fix the patchwork of state cannabis regulations or change marijuana’s treatment by the federal government as a controlled substance. But it may encourage state-chartered institutions in some states to start offering or expand cannabis banking services.

815 US FIs were “active filers” of marijuana-related suspicious-activity reports in Q1 2024, according to Financial Crimes Enforcement Network (FinCEN) data. It’s a proxy for the number of FIs with cannabis-related businesses. 6,7 Decade-old FinCEN guidance opened the door, recommending that a bank conduct due diligence that includes verifying a state license to operate a cannabis-related business, understanding the types of products to be sold and customers serviced, and monitoring for suspicious activity. 8

Sustainability

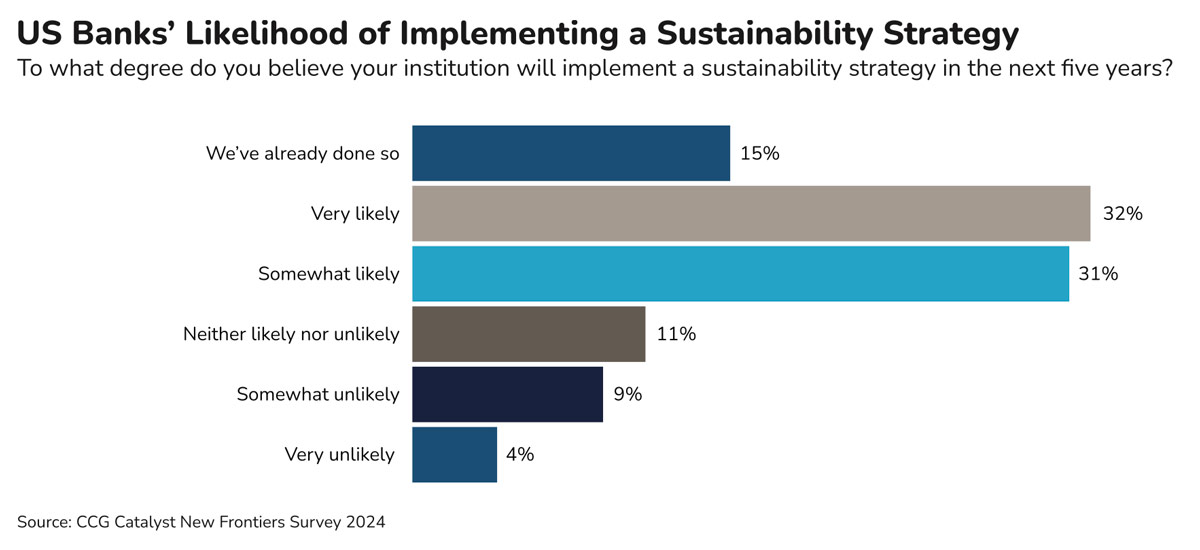

“ESG” (environmental, social, and governance) implies guidelines for corporate responsibility. The “E” of ESG is closely associated with the term as some US companies have worked to address the environmental impact of their businesses or adopted greenhouse gas goals set by the Paris Climate Agreement. 9 Differences were negligible between the results from this year’s sample and last year’s. A small number of respondents (15%) said they had already implemented a sustainability strategy, and 32% said they were “very likely” to implement a sustainability strategy in the next five years.

There are large-company blueprints for a sustainability strategy. 10,11 A sustainability strategy for a bank may include a net-zero greenhouse gas commitment between operations, supply chain, and perhaps the purchase of carbon offsets. Banks may also lend to or invest in companies that develop solutions to environmental issues, such as low-carbon energy, energy efficiency, sustainable transportation, water conservation, land use, or waste disposal.

The SEC recently adopted a rule for public companies on climate-related disclosures, which suggest how any company might consider addressing environmental risk as part of its strategy. 12 The rule requires that public companies disclose the material impacts of climate-related risks on their strategy, business model, and financial outlook, describe activities to mitigate or adapt to climate-related risks, and establish board oversight. It’s of course up to privately held banks to decide what works for them.

New technology frontiers

To enable a forward-looking business strategy, it’s crucial that bankers understand new frontiers in technology that support banking products and services. This section looks at respondents’ interest in and strategies toward different categories of tools. We take a deep dive into open banking, AI, cryptocurrency, blockchain/DLT, and real-time payments.

Open banking

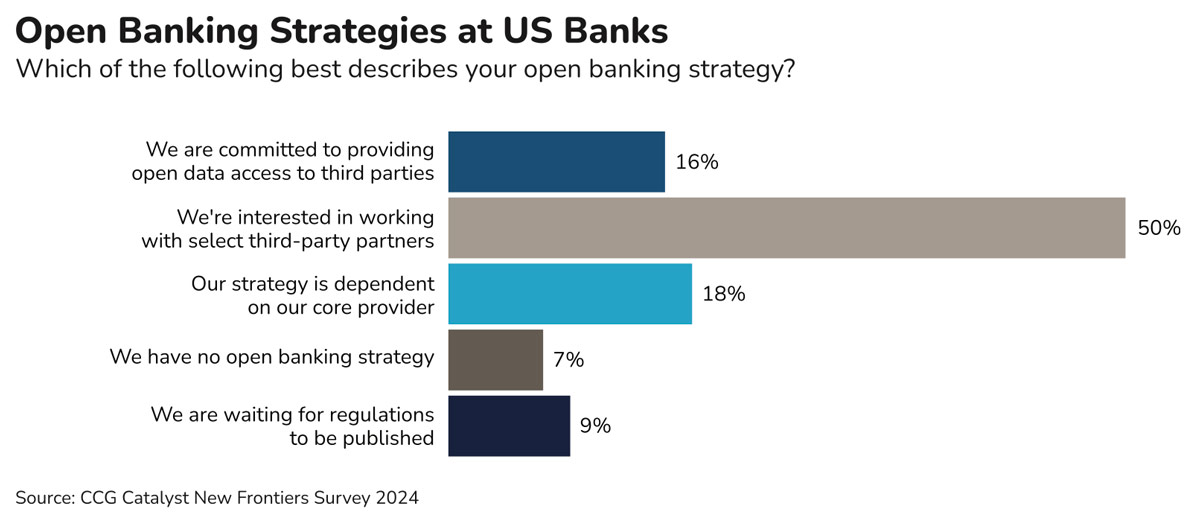

Open banking in the US refers both to the mechanism for how consumers can get secure access to their banking data for use in third-party apps and a policy solution that forces FIs to enable consumers’ use of that data. Respondents’ attitudes about open banking changed little relative to last year’s survey, even with the CFPB’s final open banking rule on the horizon. A small fraction was committed to open data access, while half of respondents said they were “interested in working with select third-party partners.” But soon, banks won’t have a choice about open banking. Those who have no strategy must move quickly to develop one.

The explosion of consumer fintech in the last decade drove consumers’ demand for features from their bank that depend on API connections to access financial data, which aggregators facilitated. 13 The policy solution is nearing completion. A rule due to be finalized shortly is expected to require all roughly 9,000 FIs in the US 14,15 to offer the APIs and developer resources for third-party services to access consumer banking data securely and robustly at consumers’ request. It will also clarify FIs’ and fintechs’ rights and obligations regarding the sharing of consumers’ financial data, including provisions for data security, risk management, and consumer privacy. If the CFPB’s rule goes into effect as proposed, it will enforce open banking for checking, savings, and credit card accounts, prepaid cards, and digital wallets. 16

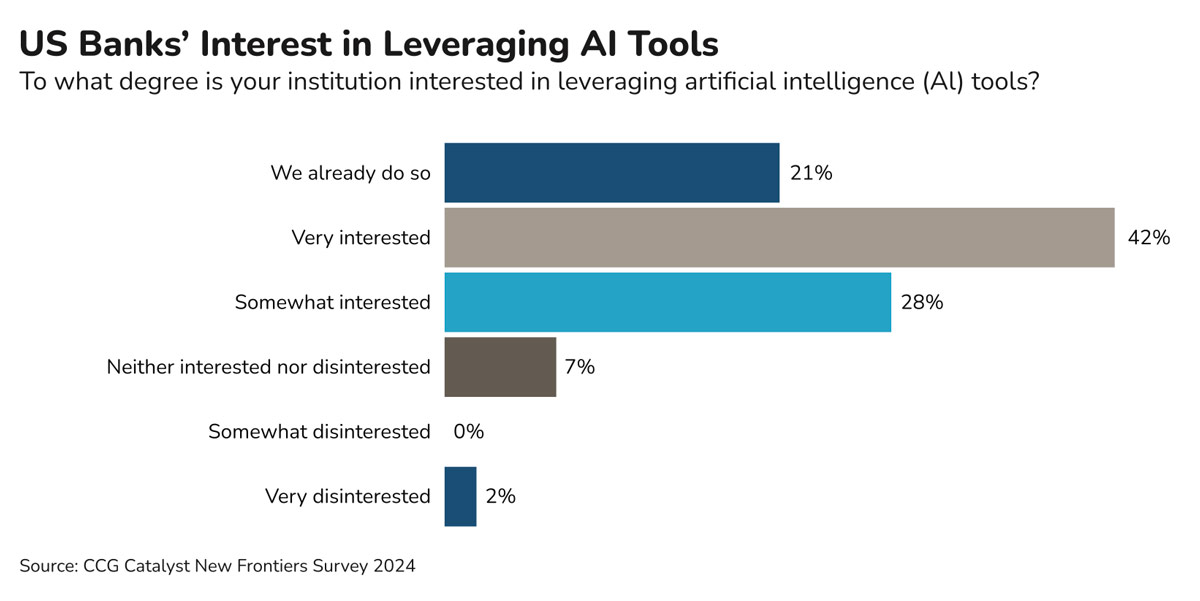

AI

The most recent AI hype, which started with the release of ChatGPT, made it top of mind among respondents for another year. The degree of interest among respondents in leveraging AI tools was exceptionally strong versus other technologies but pulled back a bit from last year’s study. The percentage of respondents who were “very interested” fell from 57% to 42%, while those “somewhat interested” rose from 19% to 28%.

The mystery and possibility surrounding what AI means in practice while AI-based branding proliferates reinforce a sense of seismic change. There is, however, a measured story to tell. AI is commonly used in banking for machine learning-driven tasks in AML, fraud detection and prevention, underwriting, analytics, biometrics, and automated document processing. On top of that, these use cases are explainable and acceptable to regulators.

Advances in AI, meanwhile, and its reach into banking applications introduce potential risk and compliance issues in addition to substantial opportunities. Bankers are aware of risks and risk mitigation related to vendor management. But at this stage, few likely have a firm idea of what specific AI-related risks are. Potential problems are acute with more complex underwriting algorithms, whose outputs are hard to explain and put banks at risk of violating compliance with fair lending rules. Algorithms’ use of too many disparate data sources may also hide illegal discrimination.

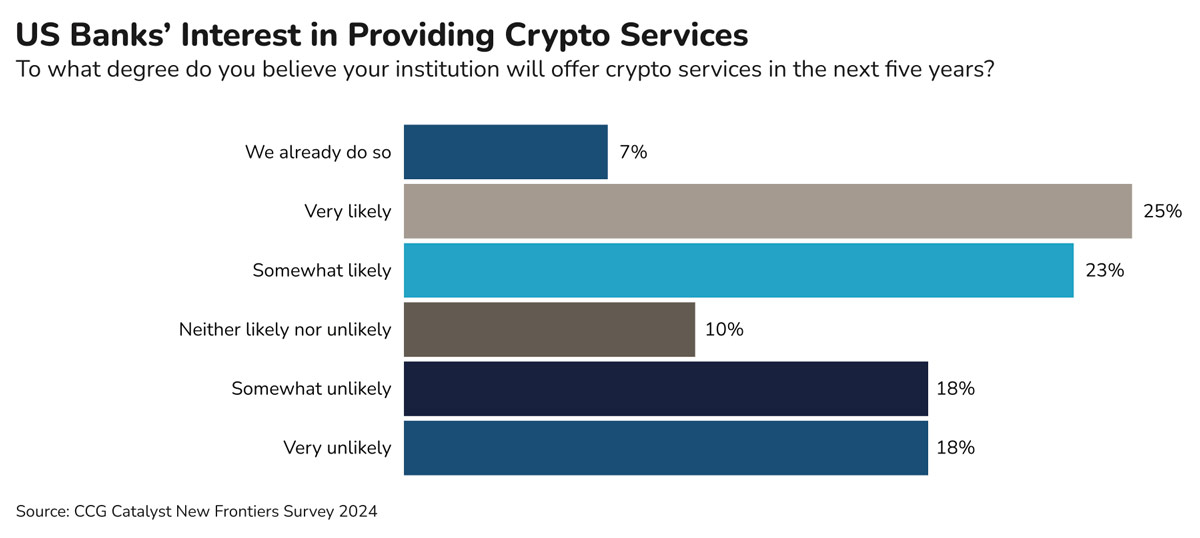

Cryptocurrency

Interest in providing crypto services may have bottomed out after crypto’s dramatic fall from grace over the past few years. With the collapse of some exchanges and crypto-friendly banks in the rear-view mirror, interest among respondents was nearly flat between the 2023 and 2024 surveys. 25% of respondents said they were “very likely” to offer crypto services in the next five years, 23% said they were “somewhat likely,” and 7% said they already did. Forty-six percent were at best ambivalent.

Now, we see crypto use cases being refined and attempts to legislate some crypto-related risk management. Proposed legislation on stablecoins has been making its way through Congress, including a House bill introduced in 2023 17 and a Senate bill introduced earlier this year. 18 The Senate bill sets general requirements for the issuance of stablecoins in the US and custodians of stablecoins, outlines disclosure requirements, and sketches out regulatory supervision of stablecoin issuers. It also “authorizes a limited-purpose State/OCC depository institution to issue payment stablecoins, with no cap on the issuance amount.”

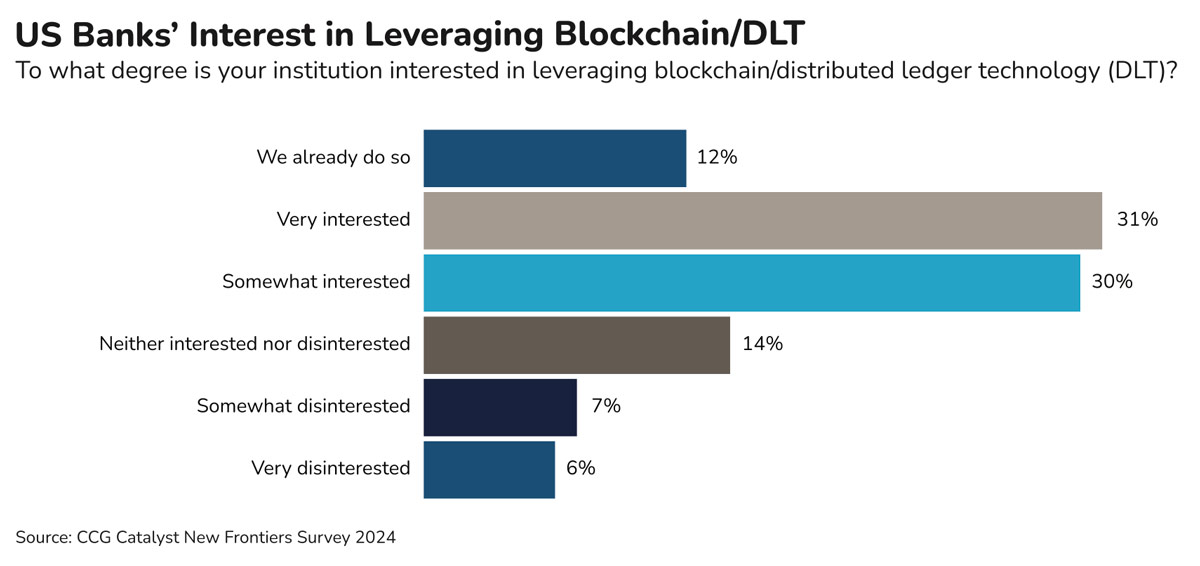

Blockchain/DLT

After riding the crypto, web3, and metaverse waves, blockchain and DLT 19 technology have settled down to long-term practical applications. The percentage of survey respondents who said they were “very interested” in leveraging blockchain/DLT fell from 38% to 31%. The number of respondents who were “somewhat interested” grew from 22% to 30%.

Blockchain is mostly in the domain of large banks, payments companies, and infrastructure providers, with applications in cross-border payments and next-generation KYC. It also promises applications that include lending and clearance and settlement systems. But productized blockchain/DLT applications in financial services are hard to find. Examples include JPMorgan Onyx, which operates a blockchain-based platform for wholesale payments, 20 and Customers Bank’s digital assets program and proprietary token 21 (the bank no longer markets them prominently 22). Top financial services applicants for blockchain/DLT patents include Bank of America, JPMorgan Chase, and Mastercard, and filings haven’t stopped. 23

Real-time payments

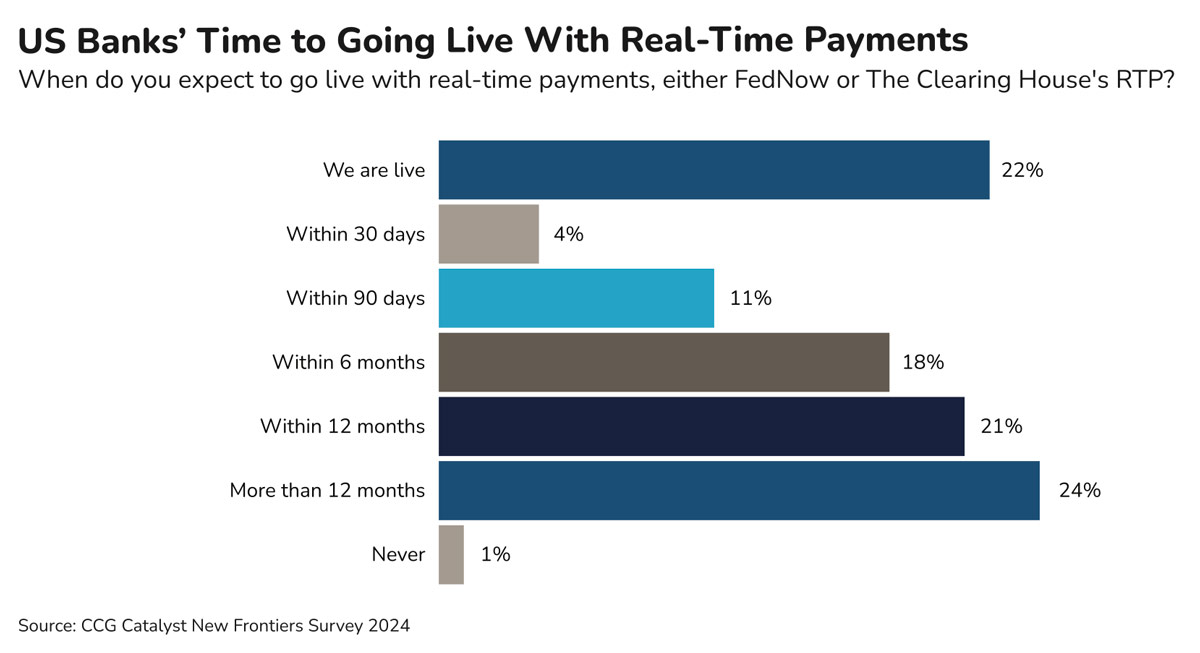

Just over a fifth of respondents said they were live with either The Clearing House’s Real-time Payments network (RTP) or the Federal Reserve’s FedNow network. Planned adoption among respondents was promising: 54% said they would go live with real-time payments within the next 12 months. There were virtually no permanent holdouts to real-time payments among respondents to the survey (1% said “never”). The next challenge is to both send and receive real-time payments. In August, nearly all the 34 certified service providers, which provide enabling technology and services, said they supported both. 24

Real-time payments in the US have been a long time coming. RTP went live in 2017, and FedNow went live in 2023. 25,26 FedNow promises the widespread adoption of real-time payments among US banks — eventually. Going live with FedNow isn’t as easy as flipping a switch. Batch-based core systems and legacy payments hubs aren’t designed to settle payments instantly, and bank staff only operating on traditional hours aren’t enough to keep a system operable all the time as promised.

Changes to technology and processes may be substantial for real-time payments. It would be an ordeal for banks that don’t have real-time technology in place or the staff that can address unique problems real-time payments pose to implement them. Changes to technology for these banks may come in the form of a real-time layer above the core that includes real-time payments functionality or a next-generation core system with real-time processing. Meanwhile, they would need staff to operate outside traditional business hours to oversee real-time fraud detection and risk assessment, address exceptions that need manual intervention, and handle technology issues.

Final thoughts

Our respondent base appears more cautious than last year, but they did not pull back as far as one might expect against the current backdrop. This is promising and suggests they’re carefully considering new opportunities. Hopefully, this will last, pushing executives to stay grounded as enthusiasm for the next big thing emerges. Evenhanded analysis, careful decision making, and a cogent strategy should rule the day.

In particular, AI presents a unique boardroom challenge because the range of applications is broad but not all well-understood, fueling hype — and still, it has well-established uses in bank technology. More advanced AI will likely be used for fraud management, compliance, security, and underwriting. But third-party risk and explainability pose potential compliance problems, and while generative AI shows promise, it’s unproven.

As bankers try to catch the next wave of innovation, it bears repeating: Study new business models and technologies carefully before pursuing them, build your organization to execute successfully on innovation strategies, and set appropriate guardrails.

Survey respondent demographics

©CCG Catalyst 2025 – All Rights Reserved

No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage and retrieval system, without prior permission in writing from the publisher.

Read New Frontiers in Banking 2023: Contemplating the Future

Download a PDF of this article